From renting spare rooms and vacation homes to car rides or using a bike…name a service and it’s probably available through the sharing economy. Taxpayers who participate in the sharing economy can find helpful resources in the IRS Sharing Economy Tax Center on IRS.gov. It helps taxpayers understand how this activity affects their taxes. It also gives these taxpayers information to help them meet their tax obligations.

https://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.png00Nathanhttps://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.pngNathan2019-04-26 10:00:302019-10-14 18:26:38Six things taxpayers should know about the sharing economy and their taxes

Now that the April tax-filing deadline has come and gone, many taxpayers are eager to get details about their tax refunds. When it comes to refunds, there are several common myths going around social media.

https://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.png00Nathanhttps://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.pngNathan2019-04-24 10:00:082019-10-14 18:27:28Don’t fall for myth-leading information about tax refunds

Tax-related identity theft occurs when a thief uses someone’s stolen Social Security number to file a tax return and claim a fraudulent refund. The victim may be unaware that this has happened until they e-file their return. Even before the victim files their return, the IRS may send the taxpayer a letter saying the agency identified a suspicious return using the stolen SSN.

https://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.png00Nathanhttps://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.pngNathan2019-04-22 10:30:412019-10-14 18:27:43ID theft: Here’s what to look for and what to do when it happens

Just like taxpayers who file their taxes by the April deadline, those who filed an extension should also do everything to make sure their tax return is complete and accurate. Errors on a tax return can mean it will take longer for the IRS to process the return, which in turn, could delay a refund.

https://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.png00Nathanhttps://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.pngNathan2019-04-18 17:18:202019-10-14 18:28:04Extension filers should avoid these errors when filing their tax return

The IRS just issued an updated publication with information for individual taxpayers and business owners unable to pay their taxes. This electronic pub, Offer in Compromise Booklet, helps people understand how an offer in compromise works.

An offer in compromise is an agreement between a taxpayer and the IRS that settles a tax debt for less than the full amount owed. An offer in compromise is an option when a taxpayer can’t pay their full tax liability. It is also an option when paying the entire tax bill would cause the taxpayer a financial hardship. The ultimate goal is a compromise that suits the best interest of both the taxpayer and the agency.

When reviewing applications, the IRS considers the taxpayer’s unique set of facts and any special circumstances affecting the taxpayer’s ability to pay as well as the taxpayer’s:

Income

Expenses

Asset equity

The booklet covers everything a taxpayer will need to know about submitting an offer in compromise, including:

Who is eligible to submit an offer

How much it costs to apply

How the application process works

The booklet also includes the forms that taxpayers will complete as part of the offer in compromise process.

1. Back-Up and Protect Your Data As the tax preparer, backing up and protecting your data should be a primary concern. Making regular backups to an external storage device at a minimum of once per week is important. Imagine next week your hard drive fails. The returns you’ve done, acknowledgement reports, PDF copies, and scanned documents are gone. Without a backup, your only hope is to take your computer to a technician who is going to charge hundreds of dollars to attempt to recover data and there is no guarantee they succeed. If they can’t recover the data, hopefully you had paper copies, but it could take hundreds of man hours reinputting data. If you don’t have paper copies, well, we hope you are lucky enough to never get audited. If you have a backup, you would only need to spend a couple hours bringing your data over and you’d be ready to go. Taxware does NOT store a copy of your data. Seek competent technical advice to keep your computers and data protected.

2. Don’t Forget to Pull in Acknowledgements

As a security measure we purge acknowledgement records every 30 days. This means after 30 days we will only be able to tell if the return was accepted or rejected, however we will not be able to read the reason why the return was rejected. If you have returns that are awaiting acknowledgement for longer than 5 days, call technical support and a technician will investigate why your acknowledgements have not come through.

3. Have Last Minute Rejects?

Don’t stress, if you get a rejected return on April 15th the IRS gives you a 3 day grace period to fix it!

4. Start your Free Trial with Textellent.com Do you want to grow your business for the 2019 Tax year? Now is the time to evaluate and start your free trial with Textellent, the text marketing and appointment scheduling platform that is fully integrated within your Wintax program. Just one short on-boarding appointment and you will be up and running. Doing this in the off-season should help you have the time to really delve into the many benefits and options this additional program could provide you and your business.

5. Celebrate! Last but not least, plan and go on vacation! You deserve it! TripAdvisor is one of our favorites.

https://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.png00adminhttps://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.pngadmin2019-04-11 21:48:592019-04-12 23:54:185 Tips To Close The Tax Season

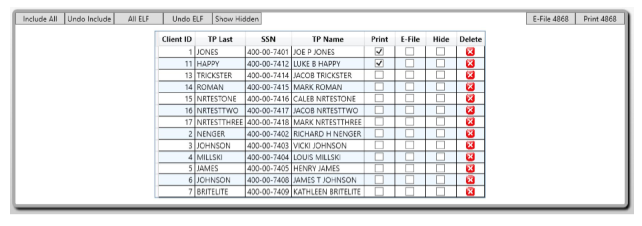

Towards the end of tax season, we field some telephone calls helping clients transmit extension form 4868 for their clients. When the telephone call is about finished the client will make a comment something along the lines of “thanks, one down 40 to go!”. It’s about that time Taxware customer support becomes their best friend when they let them know that there is an easier way to do all their extensions in a batch.

In the program we have a utility that compares your current year data folder with your prior year data folder to build a database of the tax payers you haven’t recalled and worked with yet. With this database you can send extensions in a batch. In addition to its main functions there are some other great reports and tools.

Here is a link for a step by step guide showing how to use the comparison tool and how to batch e-file extensions.

https://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.png00adminhttps://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.pngadmin2019-04-08 19:11:262020-07-07 20:32:05Client Comparison and Batch Extensions using Wintax NextGen

WASHINGTON — The Internal Revenue Service on Friday, March 29th clarified the tax treatment of state and local tax refunds arising from any year in which the new limit on the state and local tax (SALT) deduction is in effect.

In Revenue Ruling 2019-11 (PDF), posted on IRS.gov, the IRS provided four examples illustrating how the long-standing tax benefit rule interacts with the new SALT limit to determine the portion of any state or local tax refund that must be included on the taxpayer’s federal income tax return. Friday’s announcement does not affect state tax refunds received in 2018 for tax returns currently being filed.

The Tax Cuts and Jobs Act (TCJA), enacted in December 2017, limited the itemized deduction for state and local taxes to $5,000 for a married person filing a separate return and $10,000 for all other tax filers. The limit applies to tax years 2018 to 2025.

As in the past, state and local tax refunds are not subject to tax if a taxpayer chose the standard deduction for the year in which the tax was paid. But if a taxpayer itemized deductions for that year on Schedule A, Itemized Deductions, part or all of the refund may be subject to tax, to the extent the taxpayer received a tax benefit from the deduction.

Taxpayers who are impacted by the SALT limit—those taxpayers who itemize deductions and who paid state and local taxes in excess of the SALT limit—may not be required to include the entire state or local tax refund in income in the following year. A key part of that calculation is determining the amount the taxpayer would have deducted had the taxpayer only paid the actual state and local tax liability—that is, no refund and no balance due.

In one example described in the ruling, a single taxpayer itemizes and claims deductions totaling $15,000 on the taxpayer’s 2018 federal income tax return. A total of $12,000 in state and local taxes is listed on the return, including state and local income taxes of $7,000. Because of the limit, however, the taxpayer’s SALT deduction is only $10,000. In 2019, the taxpayer receives a $750 refund of state income taxes paid in 2018, meaning the taxpayer’s actual 2018 state income tax liability was $6,250 ($7,000 paid minus $750 refund). Accordingly, the taxpayer’s 2018 SALT deduction would still have been $10,000, even if it had been figured based on the actual $6,250 state and local income tax liability for 2018. The taxpayer did not receive a tax benefit on the taxpayer’s 2018 federal income tax return from the taxpayer’s overpayment of state income tax in 2018. Thus, the taxpayer is not required to include the taxpayer’s 2019 state income tax refund on the taxpayer’s 2019 return.

*This message was distributed by IRS Newswire, an IRS e-mail service. For more information on federal taxes please visit IRS.gov.

https://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.png00Nathanhttps://www.taxwaresystems.com/wp-content/uploads/2018/04/tw_logo_website.pngNathan2019-04-01 18:03:402019-04-01 18:03:40With new SALT limit, IRS explains tax treatment of state and local tax refunds